Global smartphone market sees modest growth in Q1

April 30, 2025

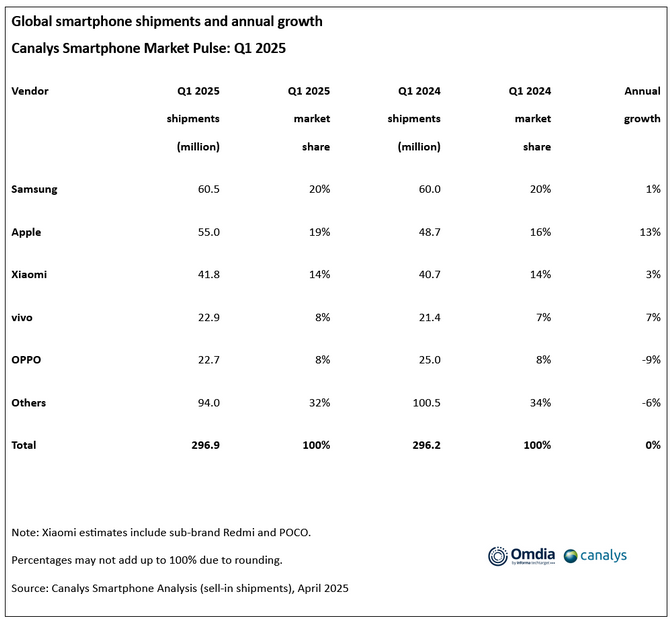

According to Canalys (now part of Omdia) research, in Q1 2025, the global smartphone market recorded a slight growth of 0.2 per cent, with shipments reaching 296.9 million units. As the peak replacement cycle came to an end and vendors prioritised healthier inventory levels, global smartphone market growth slowed for the third consecutive quarter.

Samsung maintained its lead, shipping 60.5 million units, supported by the launch of its latest flagship models and competitively priced new A-series products. Apple ranked second with 55 million units shipped and a 19 per cent market share, driven by growth in emerging Asia Pacific markets and the US. Xiaomi secured third place with 41.8 million units shipped and a 14 per cent market share, leveraging its diverse product ecosystem to strengthen its brand in Mainland China and emerging overseas markets. vivo and OPPO followed in fourth and fifth places, with shipments of 22.9 million and 22.7 million units, respectively.

“The regional smartphone landscape is becoming increasingly complex,” commented Toby Zhu, Principal Analyst at Canalys (now part of Omdia). “Markets that had shown strong momentum over the past year, such as India, Latin America, and the Middle East, are now experiencing notable declines in Q1 2025, indicating saturation in replacement demand for mass-market products. Most Android brands actively adjusted inventory levels in Q1 to avoid disruptions to new product launches and channel pricing. The European market has also dropped after a brief recovery, with vendors facing high flagship inventory from late last year and disruptions in mid- and low-end product lines due to the upcoming eco-design directive. Nonetheless, some regions are still demonstrating strong demand. Government subsidy programmes stimulated Mainland China’s growth, while Africa continued to benefit from vibrant retail activities and proactive market expansion efforts. Vendors can still expand by optimising their product portfolios in this complex regional environment. For instance, vivo and HONOR achieved double-digit growth in their overseas markets, with HONOR reaching a historic high in its overseas shipments.”

“The US smartphone market stood out, growing 12 per cent year on year in Q1, primarily driven by Apple,” said Le Xuan Chiew, Research Manager at Canalys (now part of Omdia). “Apple proactively built up inventory ahead of anticipated tariff policies. While iPhones produced in Mainland China still account for the majority of US shipments, production in India ramped up toward the end of the quarter, covering standard models of the iPhone 15 and 16 series, alongside accelerating production of the 16 Pro series. With ongoing fluctuations in reciprocal tariff policies, Apple is likely to further shift US-bound production to India to reduce exposure to future risks. Tariffs are also expected to disproportionately impact entry-level devices, potentially reducing the availability of lower-cost models and driving average selling prices (ASPs) higher in the US. These dynamics introduce new uncertainties not only for Apple but also for Android brands competing in the market. Pricing strategies, operator bundling packages and future product structures will come under significant pressure. Meanwhile, the US smartphone market is expected to experience considerable volatility over the next two to three quarters, impacted by inventory corrections and weakening consumer confidence.”

“Major smartphone brands have not yet adjusted their full-year shipment targets, despite the lackluster performance in Q1,” continued Zhu. “They remain optimistic about a market rebound in Q2 and in the second half of the year. Some regions, such as Southeast Asia and Latin America, already showed signs of gradual recovery in March. Additionally, decreasing inventory levels and the mid-year launch of new mid- and low-end products have boosted their confidence. However, vendors still face multiple challenges. First, brands are adopting a cautious approach to hardware upgrades in mass-market segments to offset rising costs, necessitating more refined management of product life cycles, pricing and go-to-market strategies. Second, competition in the mid-range ($200 to $400) segment will intensify as brands seek breakthroughs in ASPs. Third, the possibility of escalating global trade tensions could drive more countries to pursue localized smartphone manufacturing, posing additional investment and cost pressures for vendors.”

Other posts by :

- Russian satellite tumbling out of control

- FCC boss praises AST SpaceMobile

- Rakuten makes historic satellite video call

- Rocket Lab confirms D2C ambitions

- Turkey establishes satellite production ecosystem

- Italy joins Germany in IRIS2 alternate thoughts

- Kazakhstan to create museum at Yuri Gagarin launch site

- AST SpaceMobile gets $42 or $1500 price target

- Analyst: GEO bloodbath taking place